The Future of Cash: Iceland vs. Sweden

JP Koning

JP Koning 2 Comments

2 CommentsThis blog post is a guest post on BullionStar’s Blog by the renowned blogger JP Koning who will be writing about monetary economics, central banking and gold. BullionStar does not endorse or oppose the opinions presented but encourage a healthy debate.

The poster child of a cashless society is Sweden. There are all sorts of anecdotes about beggars accepting cards, churches passing around mobile payments devices instead of collection plates, and banks no longer providing customers with cash. It is no wonder then that Sweden is the only country in the world to show a decline in banknotes and coins in circulation, the quantity of cash outstanding having fallen from 109 billion SEK in 2006 to 56 billion SEK in 2018. If you want to read more, I wrote about the Swedish miracle on my Moneyness blog here.

The death of cash scenario portended by Sweden is contradicted by another Nordic nation, Iceland. If Sweden is close to the forefront of the cashless revolution, Iceland is not only ahead of it but at the very front of the pack. No country does more point-of sale payments per capita than Iceland, clocking in at 426.9 in 2016. Whereas Sweden has an incredibly low cash-to-GDP ratio of around 1.75% , Iceland was already all the way down to an impressive 1.2% by the early 2000s! (The cash-to-GDP ratio is the number of banknotes and coins outstanding at the end of the year divided by yearly GDP. I get these numbers here).

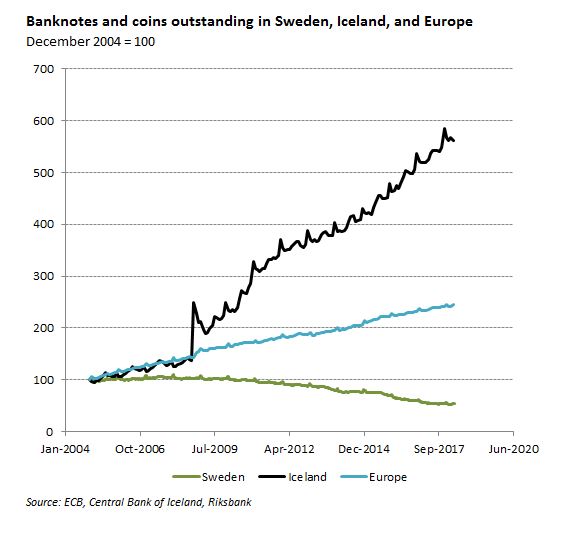

One would probably be safe in assuming that, like Sweden, Iceland is characterized by a steady decline in banknotes and coins outstanding. But this isn’t the case, as the chart shows below.

Not all Scandinavian countries are going cashless. You can see precisely when Icelanders lost trust in their banks and began cashing out of deposits into notes. pic.twitter.com/fN0i1dY9s7

— JP Koning (@jp_koning) March 12, 2018

Since the 2008 credit crisis, Iceland has seen a tremendous resurgence in the demand for cash. Not only is the rate of growth in króna notes and coins in circulation far exceeding that of Sweden, but as the chart below illustrates, it is also far ahead of euro cash growth. As for Iceland’s cash-to-GDP, it has doubled to around 2.4% since the crisis, which means that the island nation is now more cash intensive than Sweden.

What is happening? It may be useful here to borrow from a recent Bank for International Settlements (BIS) paper Payments are a-changin’ but cash still rules and differentiate between means-of-payment and store-of-value demand for coins and banknotes. It is unlikely that the resurgence of Icelandic cash demand is due to payments needs. Rather, I’m going to show that it is probably due to the latter type of demand, store-of-value. This sort of demand occurs when people indefinitely lock away a few extra bills in a safe as opposed to putting them in their wallets for tomorrow’s grocery run.

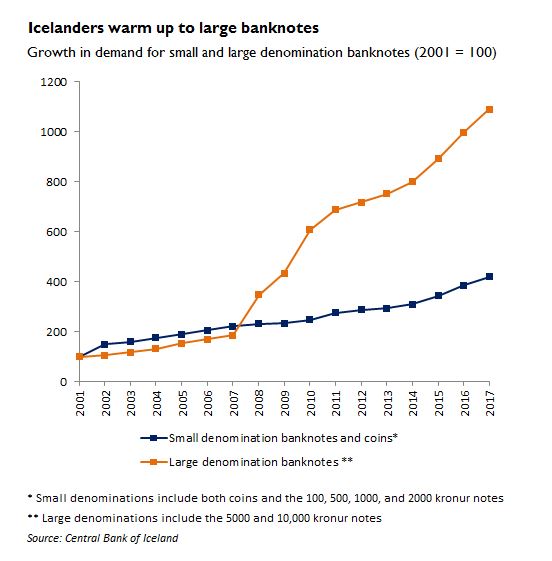

The easiest way to try and determine when cash is being held as a store-of-value or a means of payment is to observe the denomination structure of coins and banknotes. In theory, larger-denomination notes, which are less cumbersome, are mostly held as a store of value whereas smaller ones will tend to be used in payments. Below I’ve charted the evolution of Iceland’s denomination structure over time.

You can see that growth in low-denomination banknotes and coin slightly exceeded growth in higher denomination notes until the 2008 financial crisis, at which point the demand for high denomination banknotes exploded. In 2013 the Central Bank of Iceland even introduced a new note, the 10,000 krónur (currently worth around US$96), to meet Icelander’s growing store-of-value requirements.

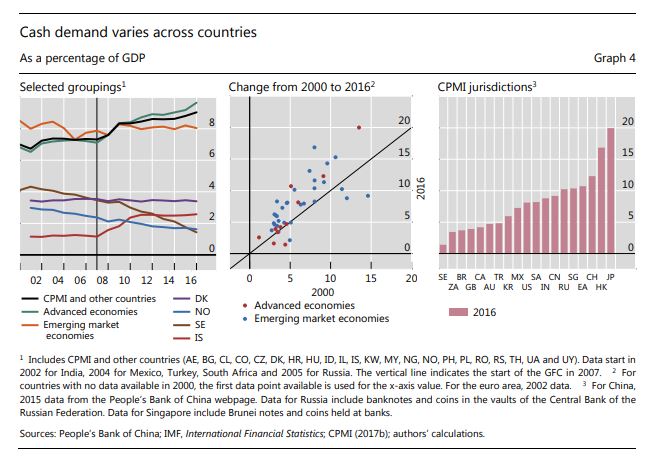

According to the BIS paper, one factor that drives the demand for notes as a store of value is the level of interest rates. If you choose to hold cash, you’re losing out on interest, but the lower the interest rate the smaller your loss and the more attractive a large-denomination banknote gets. Indeed, the BIS report finds that lower interest rates all across the world explain a large part of the post-crisis global thirst to hold high denomination banknotes like the €500 note, 1000 Swiss franc, ¥10,000, or US$100, as illustrated in the chart below. This may be the case in Iceland too, since rates have fallen quite a bit since 2008.

Iceland is somewhat unique because of the terrific damage sustained by its banks during the credit crisis. All three–Kaupthing, Glitnir, and Landsbanki–went bankrupt. Prior to the crisis Landsbanki had established a banking presence in the UK and Netherlands. Iceland’s government refused to meet its deposit insurance commitments for these foreign customers while protecting Icelanders. The crisis revealed that the safety of both Iceland’s banks and its deposit guarantee scheme were less assured than most had previously thought. This may explain some of the explosion in hoarding of Icelandic banknotes. Notes, after all, are a direct promise of the government and are free from the sort of default risk that bedevils a private deposit.

In addition to having a financial incentive to hold more banknotes, Icelanders also have emotional reasons for doing so. They are resentful of bankers, who are rightly viewed as the ones most responsible for placing Iceland in such a precarious position on the eve of the ’08 financial crisis. Some 26 bankers have received sentences of up to five years, which makes Iceland the only nation to have imprisoned bankers for their role in the crisis. The country has even flirted with the idea of sovereign money, a monetary system in which private banks can no longer issue money, abdicating that role to the the state.

In this context, it is no wonder that demand for high denomination banknotes is growing. Angry Icelanders can register their protest votes against the banking system by storing five 10,000 kronur notes under their mattress for a rainy day instead of holding 50,000 krónur in a low-yielding savings account.

To sum up, Iceland and Sweden are both leading the world in digital payments. Yet while Sweden hints at a world in which digital payments lead to cash’s demise, Iceland tells us something different. Even in a world where everybody pays with a card or an app, people may still want access to old-fashioned cash. First, banknotes and coins are still useful in a number of payments situations, say when payments systems have gone down or in coin-operated laundry machines. In Iceland’s case, this is confirmed by continued growth in small-denomination banknotes and coins outstanding, which are keeping up with GDP growth.

But even more importantly, Iceland shows that banknotes–in particular large denomination ones–are a universally available ultra-safe investment. It took a crisis for this to be evident, since when times are normal people are quite content to hold riskier bank-issued claims on banknotes. Other government instruments like t-bills and bonds also provide the same degree of safety as a banknote. But these require a degree of financial sophistication to purchase, and are thus less accessible than cash, which is widely available and easy to buy.

As policy makers navigate the future of cash, in particular that of high denomination banknotes, the Swedish model has become a much discussed benchmark. But it would be irresponsible of policy makers if they failed to consider its fellow Nordic nation, Iceland, as an equally informative model.

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Life Under a Gold Standard

Life Under a Gold Standard

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization