Singapore, Brunei, and the $10,000 Banknote

JP Koning

JP Koning 5 Comments

5 CommentsIn 2014, Singapore stopped printing the mammoth S$10,000 banknote, one of the world’s largest value banknotes, citing “risks associated with large value cash transactions." Although it is no longer being printed, the S$10,000, which is worth around US$7,400, remains in circulation and continues to be accepted as legitimate legal tender. But once deposited in the banking system, all S$10,000 notes will be returned to the Monetary Authority of Singapore (MAS)—the institution responsible for issuing notes and setting monetary policy—to be destroyed. With no new ones being created, the supply of S$10,000 can be expected to steadily shrink.

The title of world’s highest-denomination banknote in production now passes to neighboring Brunei, which issues the B$10,000, also worth about US$7,400. Brunei, a small nation on the island of Borneo with a population of 450,000, is the world’s fourth richest country (ranked by GDP per capita) thanks to its oil & gas reserves. Interestingly, due to a long financial relationship between Brunei and Singapore, Brunei dollars are considered to be “customary tender" in Singapore (more on that later). So even as the S$10,000 is slowly phased out, the B$10,000 may still have a backup role to play.

Singapore and Brunei have an agreement—the Currency Interchangeability Agreement—dating back to 1967 which obligates the monetary authority of each nation to accept the banknotes of the other nation at par with their own currency. Private Singaporean banks can thus safely accept Brunei dollar notes for deposit, knowing that the MAS will not only buy these foreign notes at a one-to-one rate with Singapore dollars but will do so without charging a fee. Vice versa with Bruneian banks.

MAS ships all the Brunei paper dollars it receives back to Brunei. Likewise, the Autoriti Monetari Brunei Darussalam (AMBD), Brunei’s monetary authority, flies Singaporean dollars back to Singapore. According to this 2017 article, MAS has sent some B$1.3 billion annually to AMBD over the last three years. This is actually quite a lot of cash. Recent data from the AMBD shows that there is only about B$1.26 billion worth of Brunei banknotes and coins in circulation, most of this in the form of the B$100 note. Given that B$1.3 billion is shipped back each year to Brunei, the entire stock of banknotes circulates through Singapore once-a-year. Incredible!

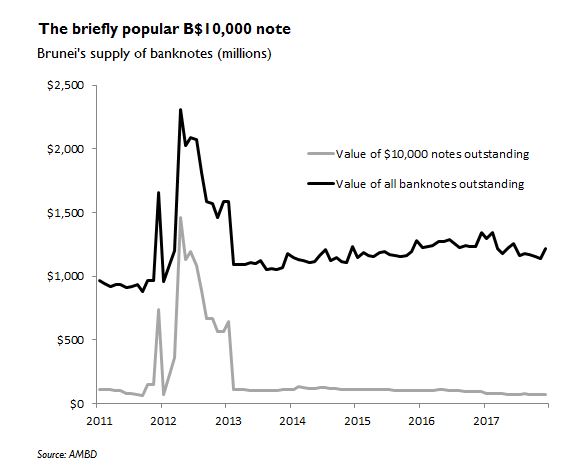

While the B$100 note is the most popular Bruneian denomination, this hasn’t always been the case. Through late 2011 and 2012, demand for the gigantic B$10,000 note exploded to B$1.5 billion, up from its regular level of around B$50 million. This spike was so marked (see below) that the entire supply of Bruneian banknotes effectively doubled, a situation that lasted until 2013 when a large quantity of B$10,000 banknotes were redeposited into the banking system. There is no indication what caused this pattern.

As I mentioned earlier, the Singapore-Brunei Currency Interchangeability Agreement describes each counterpart’s banknotes as “customary tender", differentiated from “legal tender." In Singapore, all currency notes and coins issued by the MAS are deemed legal tender. This means that any debt or transaction can be settled using MAS-issued banknotes, although if a payee (the person taking a payment) notifies a payer ahead of time, they can choose to avoid using legal tender and settle on an alternative means for transacting, say gold or euros. Since Brunei dollars are only customary tender, there is no default legal obligation on the part of retailers to accept them.

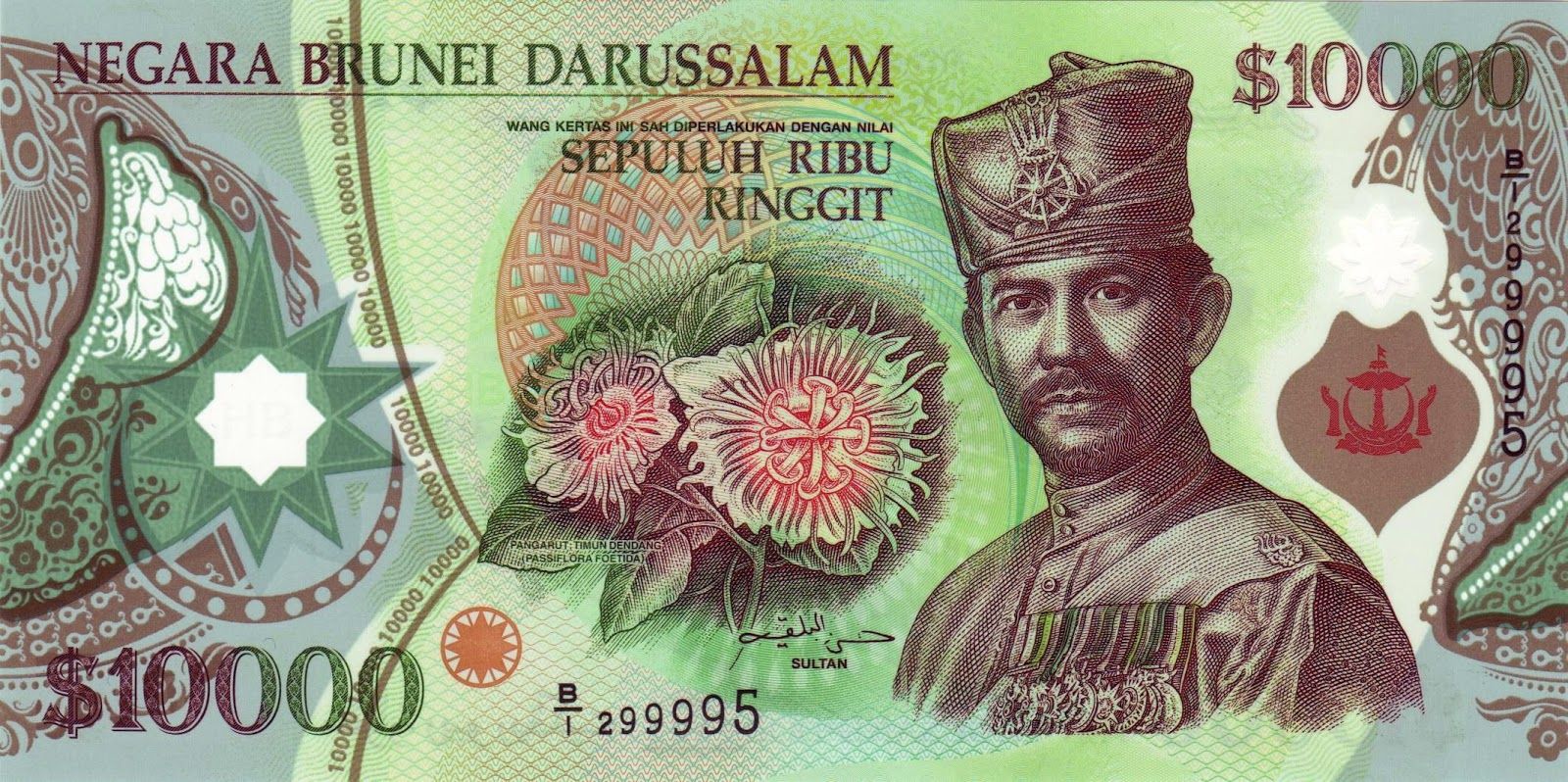

Modern $10,000 Brunei banknote

Modern $10,000 Brunei banknote

While many retailers in Singapore accept Brunei dollars, not all do. Offending retailers can be reported to MAS. And when they are reported, they usually comply. Presumably this acceptance isn’t forced on retailers, since Brunei dollars aren’t legal tender, but is asked of them in good faith. Come on guys, take one for the team.

The monetary relationship between Brunei and Singapore is an old one. Prior to their independence, Malaysia, Singapore, and Brunei were all members of British-run currency board, the Board of Commissioners of Currency, Malaya, which issued Malayan dollar banknotes. The Board of Commissioners was initially established in 1899 by the British colonial authority. A currency board is a monetary system in which the issuer of banknotes (and deposits) maintains a 100% reserve for the liabilities it has issued. In the case of the Malaya currency board, this reserve consisted entirely of assets denominated in British pounds. The advantage of a 100% reserve is that there is no way that the peg can break, so investors needn’t worry about exchange rate fluctuations.

Already merged on a monetary level, Malaysia and Singapore embarked on a post-independence political merger in 1963, but this political union fell apart in 1965. Ongoing distrust of the Malaysian administration by Singapore led to the abandonment of the currency board arrangement in 1967, with Malaysia, Singapore, and Brunei all issuing their own currencies for the first time. The three then drew up the Currency Interchangeability Agreement, obligating each to accept the others’ banknotes at par, but Malaysia dropped out in 1973, leaving Brunei and Singapore. And this is how things stand to this day.

While the Singapore dollar is no longer based on a currency board—the MAS operates what is referred to as a managed float regime—the Brunei dollar continues to be operated on the principles of the old currency board. Rather than pegging to the British pound, the AMBD fixes the Brunei dollar against the Singapore dollar. However, the AMBD does not operate an orthodox currency board because it maintains a slightly-less-than full reserve of Singaporean dollar assets.

The monetary relationship between Singapore and Brunei constitutes a currency union, much like the Eurozone. In the same way that the European Central Bank calls the shots for the group of euro-using nations, the MAS is in charge of the Singapore dollar zone. Brunei is a passenger in this relationship, much like how Greece is along for the ride in Europe. Put differently, whereas Greece imports the monetary policy of a much more powerful authority, the ECB, Brunei imports Singaporean monetary policy.

Which brings us back to the $10,000 note. The denomination structure of Bruneian coin and note issue is the one bit of monetary sovereignty that Brunei gets to control. And since the Interchangeability Agreement obligates Singapore to accept all Brunei banknotes, Singapore effectively imports the denomination policy of its smaller neighbour. The $10,000 note is dead, long live the $10,000 note!

To understand the history behind the Brunei-Singapore monetary relationship, I relied on the following sources:

- MAS Macroeconomic Review, April 2017. Pgs 73-76 [link]

- The Malayan Currency Board, 1938-1967. By Josephine George, 2016 [link]

- The Dissolution of a Monetary Union: The Case of Malaysia and Singapore 1963–1974. By Catherine Schenk, 2013 [link]

- Second separation: Why Singapore rejected a common currency with Malaysia. The Strait Times, May 24, 2016 [link]

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Life Under a Gold Standard

Life Under a Gold Standard

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization