Why Are Gold & Bonds Rising Together?

JP Koning

JP Koning 4 Comments

4 CommentsIn a previous post I mentioned that when I first broke into the financial industry, the owner of the brokerage where I worked was a dyed-in-the-wool gold bug. Most of his portfolio was invested in gold (he even owned a gold mine) and he was a supporter of the gold standard. When the market quietened down at the end of the day, he’d often reminisce about the 1970s, his favorite decade.

According to my boss’s story, he’d spent much of the 1970s buying gold futures contracts and shorting bonds. This was a fantastically profitable set of trades to make back then. With inflation crushing bond prices, my boss’s short position was paying off. And as investors flocked to gold as a hedge, the yellow metal rose from the double digits to above $800, buoying his long position. He’d built his brokerage using the profits.

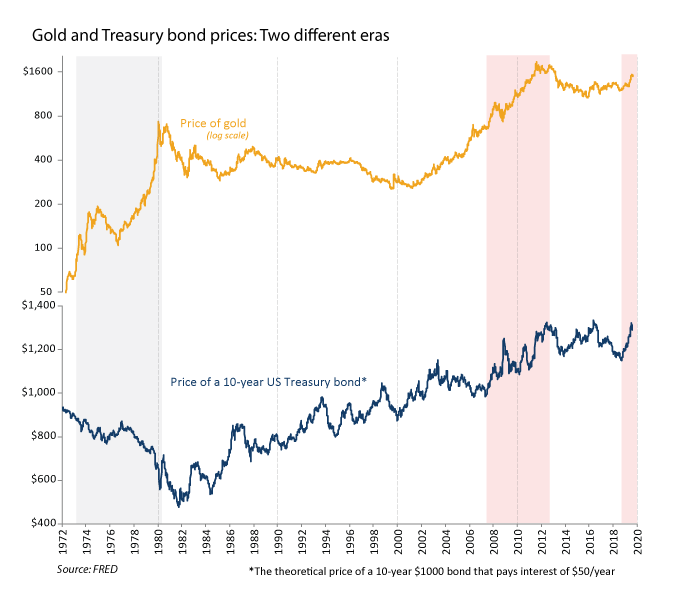

This trade had been so successful that my boss kept trying to replicate it in the 1980s and 90s. Without much success. By then central bankers had pretty much tamed inflation. Starting in 1980, the gold price would stagnate for over two decades. Meanwhile, bond prices entered a permanent bull market. (See chart below). My boss’s losses mounted.

When gold eventually bottomed in 2001, my boss’s gold futures contracts finally started to payoff. The 70s are back, he would cackle. But the other leg of the trade, short bonds, wasn’t working. Rather than collapsing as they had in the 1970s, bond prices held strong. When the 2008 credit crisis hit, the bond bull market returned with a vengeance as prices rose. Staring at his screen, my boss would mutter darkly to himself as each gain in gold was cancelled out by another whopping loss on his bond shorts.

That 70s show

My boss wasn’t the only one to find this pattern perplexing. Many financial professionals who had come of age in the 1970s were confused by the 2000s. This baby boomer cohort tends to rely heavily on an inflation-based mental model of financial prices. The model worked well in the 70s, and they’ve never forgotten it.

It goes like this. An unexpected rise in the inflation rate pushes the price of gold higher, offering gold investors a degree of protection. But not bonds. Bond interest payments and principle are fixed. Unexpectedly high inflation means that the interest rate that is paid on existing bonds is no longer high enough to compensate investors for the risk they are taking. And so the market price of existing bonds falls. New bonds will be issued with higher interest rates attached to them in order to make up for the jump in inflation.

Applying this simple model, if gold prices are observed to be rising, it’s because inflation is increasing. And if inflation is rising, bond prices should be falling. The bastards shouldn’t be moving together, my boss would rail at his trading screen throughout 2010 and 2011. It’s only a matter of time before the bubble bursts!

This year brought back memories of my boss’s vexation in the years both during and after the credit crisis. Since August 2018, the price of gold has jumped from under US$1200 to over US$1500. At the same time, global bond prices, which had been falling for several years, have been galloping higher. If he was still around, my boss would have been apoplectic.

Why do bond prices and gold prices sometimes move opposite of each other (as they did in the 1970s) but at other times move together (as they are now)?

A millennial model

To see why, we need to step beyond my boss’s 1970s-era inflation model. Let’s start out with a basic axiom. Like any asset, the price of gold has to rise at the real interest rate. The real interest rate is the inflation-adjusted return that any investor expects to earn by investing their capital.

Why does gold have to rise at the same pace as the real interest rate? If it doesn’t, then investors have the opportunity to make massive profits.

Say that the real rate of return on a bond is 5%. If gold is rising at a just 4% per year, then an investor can profit by selling the low-return asset short, in this case gold, and buying the high-return asset, bonds. They start by borrowing x ounces of gold and selling it in the market. With the proceeds they buy a 1-year bond and over the course of the year collect 5% interest. At the end of the year the bond principle is returned. Using the proceeds and interest income, the investor repurchases x gold ounces and pays back he/her short. Because the price of gold has only risen by 4% over the interim, but the investor has earned 5% from the bond, they get to keep the extra 1% as profit. Voila, risk free profits!

On the other hand, say that gold is rising 6% per year, faster than the interest rate of 5%. In this case, everyone would want to hold only gold! An investor would now do the opposite set of trades. They’d raise $x by issuing bonds, buy gold, hold the yellow metal as it shoots up by 6%, sell it, and with the proceeds pay interest of 5% and repay the bond principle. As before, the investor gets to keep the extra 1%, effectively ending up with more resources than he/she started out with.

In a competitive market, extra profits such as these can’t exist for very long. Speculators will compete them away. And so the price of gold will be set at just the right level such that the expected rate of appreciation on gold is in line with the return on bonds. That way there is nothing to choose in the way of advantage between the two assets.*

Gold and bonds do the two-step

Having set the stage, we can now start to understand how the prices of gold and bonds can simultaneously decline.

Imagine that the world begins to stagnate. Perhaps some sort of epidemic spreads across the world, cutting into everyone’s ability to produce. Capital invested in projects is now less productive. If capital is less fruitful, it won’t be able to yield as high a return as before. And so the required interest rate on bonds falls, say from 5% to 2.5%. Bond yields and bond prices always move in opposite directions, so bond prices will rise. Think about it this way. If rates fall to 2.5% then already-existing bonds that still pay the legacy rate of 5% are now worth more, and so investors will bid their price up.

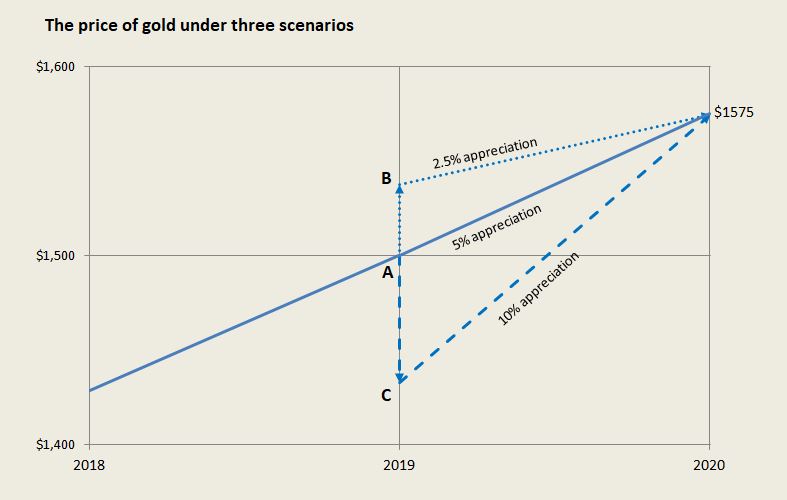

Now let’s see what happens to the price of gold when an epidemic hits. Prior to the epidemic, gold was expected to rise at the bond rate of interest of 5% a year. So from an opening price of $1500 it was expected to close the year 5% higher, or up $75, to $1575.

With the epidemic cutting the return on bonds to 2.5%, gold’s 5% return is suddenly superior. But only for a moment. Investors hungry for extra profits will quickly bid the price of gold up by $37.50 to $1537.50. At this new level the yellow metal no longer provides a superior return. Starting from $1537.50 it will still rise to hit the same level as before, $1575, by the end of the year. But this trajectory is much more muted, emulating the same 2.5% return as a bond.

So an epidemic and the stagnation that it breeds causes bond yields to fall from 5% to 2.5%. Bond prices rise. The epidemic simultaneously sends the price of gold up to $37.50, from $1500 to $1537.50. This is illustrated in the chart below. The gold price immediately jumps from A to B. It then proceeds to appreciate for the rest of the year at the more relaxed rate as captured by the dotted line.

We can also think about the opposite of an epidemic, say some significant technological breakthrough that makes capital more fruitful.

Bonds now need to provide a higher interest rate than before, say 10%. So the prices of existing bond that pay the old rate of 5% will fall. Gold, which had up till now been expected to appreciate from $1500 to $1575 in order to provide an implicit yearly rate of return of 5%, now offers investors inferior return. As they rush to dump the yellow metal, investors will bid its price down to $1435 or so. At this level it will once again be competitive with bonds. After all, if gold’s one year trajectory is from $1435 to $1575, that’s a 10% return.

This is illustrated in the chart above by a quick fall from A to C, and then a much steeper rate of appreciation through the rest of the year along the dashed blue line.

In summary

And that explains why the prices of gold and bonds sometimes move together, and sometimes diverge. When real changes to the broader economy occur (i.e. changes in technology, productivity, population growth, etc), the prices of gold and bonds tend to move together. Inflation, which doesn’t have much of an effect on real factors like productivity or growth, sets off a set of opposed reactions in these two markets. The prices of bonds and gold move in different directions.

Because my boss’s earliest financial experiences bred in him a tendency to see inflation everywhere, he was left scratching his head after the credit crisis. The price of gold consistently rose along with the price of bonds rather than varying with them. What was probably happening underneath was a decline in the fruitfulness of capital, and this was being reflected in overlying gold and bond prices.

As for the last twelve months, there are still many old timers who will no doubt claim that the rise in the gold price to $1500 is a sign of imminent inflation. But the concurrent rise in bond prices should put that suspicion to rest. It ain’t the ’70s anymore.

*There are a few caveats to the rule I’ve just described. First, we need to adjust for risk. Gold might have to appreciate a bit faster than the long term interest rate because it needs to compensate investors for being the riskier of the two. It is also more expensive to store. Investors will need to be compensated for storage costs with a bit of extra price appreciation. But the general principal stands. In equilibrium, all risk-adjusted asset returns are equal.

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Life Under a Gold Standard

Life Under a Gold Standard

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization