Gold at All Time Highs amid Physical Gold Shortages

Ronan Manly

Ronan Manly 0 Comments

0 CommentsSince 25 November when then US president elect Donald Trump first threatened to impose import tariffs on Mexico, Canada and China ( see “Trump Tariffs will Trigger Global Trade War, with Gold and Silver Set to Benefit“), gold markets in New York and London have been signalling fears that these tariffs would include gold and silver imports from Mexico and Canada.

These fears have now been fully confirmed, since on Saturday 1 February, Trump has gone ahead and signed Executive Orders imposing “a 25% additional tariff on imports from Canada and Mexico and a 10% additional tariff on imports from China”, with the tariff impositions set to come into effect on Tuesday 4 February. Given that the only concession in these Executive Orders is a lower 10% tariff for Canadian energy resources, and with no explicit exemptions for precious metals, it is presumed that a 25% import tariff applies to all gold and silver bullion imports coming from Mexico and Canada. That includes precious metals doré and precipitates, and refined bullion in the form of bullion bars and coins.

A 25% tariff on gold imported from Mexico or Canada will therefore add $700 per oz to the international gold price, assuming a $2800 gold price, and leave the final price post tariff at a staggering $3500 per oz. All of this is also taking place in an environment in which gold prices have yet again reached new all time highs, with a highest daily close and a highest monthly close registered on the last day of January.

Market Reactions to Tariff Expectations

Before looking at the implications of what the import tariffs will mean for precious metals going forward, it’s instructive to look at what impact the “anticipation of tariffs" has already caused. While the below looks at COMEX gold, the situation is similar for COMEX silver.

Following Trump’s late November threats of tariffs, fears of higher import prices triggered a panicked rush to import physical gold into the US, with traders on COMEX bidding up gold futures prices to ensure they had exposure to sufficient gold deliverable in the US. This surge in price in turn forced short sellers to cover their positions, all of which drove COMEX prices higher than the LBMA London spot price. As the COMEX-London spread widened, London traders then also scrambled to transport more gold to New York so as to take advantage of the arbitrage opportunity.

Since late November 2024, nearly 400 tonnes of gold has flowed into the vaults of the COMEX in New York and surrounding areas, with total COMEX gold inventories rising from less than 20 million ozs to nearly 32 million ozs. Since Trump’s tariff threats were first made public, the COMEX-London gold price spread has widened on a number of occasions, first notably for a few weeks in early December, and then again significantly in January amid renewed concerns that the tariffs would be imposed by as early as 1 February. For example, on Friday 31 January, the COMEX April futures gold price was trading at $2862, a full $64 above the London spot close price of $2798.

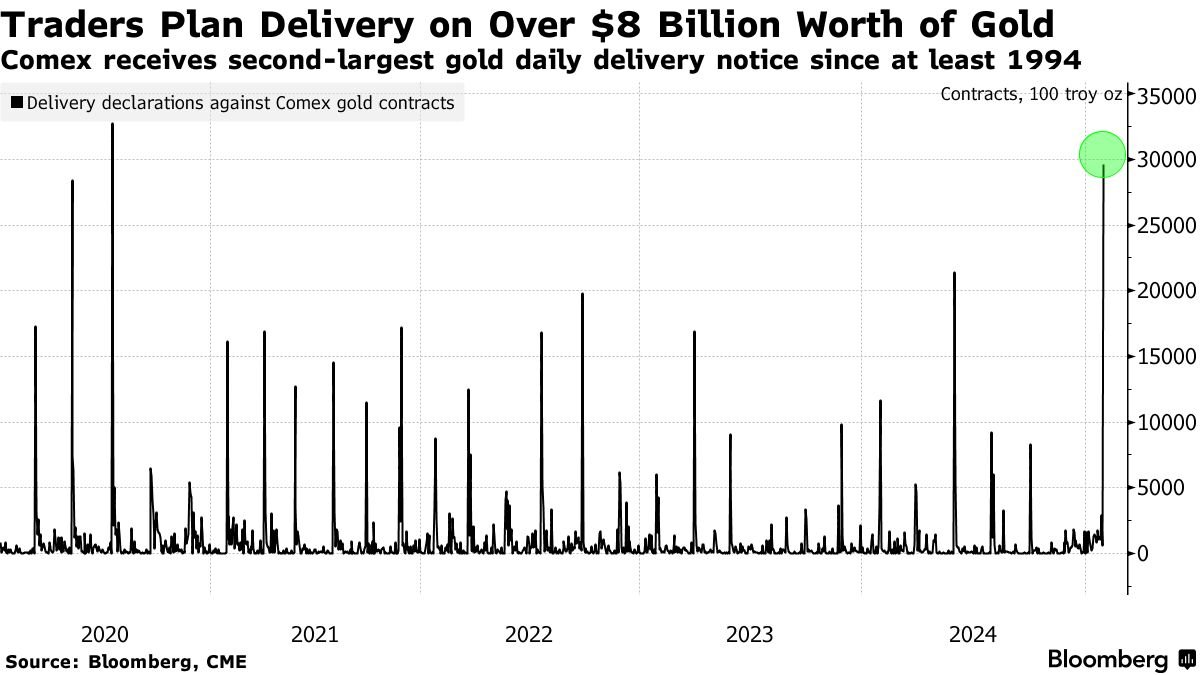

Record gold deliveries on COMEX

To illustrate the current scramble for physical gold on COMEX, the most recent delivery data is eye opening, with the Exchange seeing the second highest ever number of contracts moving to delivery on a ‘first delivery date’ which was 2,962 million ozs, or 92 tonnes, for the February contract (first delivery is Monday 3 February). This means ownership of this metal changes hands between long contract holders (who take delivery) and short contract holders (who make delivery). Of that total, JP Morgan has to deliver 1,485 million ozs (46 tonnes) worth over $4 billion.

A record number of delivery transactions on first delivery date signals strong physical demand and a preference for physical metal over paper positions, since long holders have not rolled their contracts, but have decided to wait and get their filled via delivery. The surge in deliveries has also continued for “second delivery date” (4 February), with another 11,028 contracts moving to delivery. That’s 40,649 contracts in total just for the first 2 days of February, and represents 126 tonnes of gold worth $ 11.38 billion.

While gold imported into the US and entering the COMEX vaults is transparent to an extent since it shows up on CME gold vault reports, its important to remember that this is only part of the story, since other gold is being imported to the US into private vaults that is harder to track.

US importing gold directly from Switzerland and the UK

The US is now hoovering in staggering quantities of gold bullion from countries that it normally exports gold to, driven by – the now correct – expectation of tariff impositions on bullion.

While both Switzerland and the UK had been, up to recently, by far the two largest export markets for US gold bullion, now the flows are going in the opposite direction, and in far greater magnitudes. In December 2024, Swiss gold exports directly to the US surged to 64.5 tonnes, an 11 fold increase on the previous month, and the highest monthly total since March 2022. Likewise, Swiss gold is also getting routed to United Kingdom (which really means London) and then sent out from London to the US. In December, Swiss gold exports to London also surged 14.3 tonnes, from 1 tonne during the previous month.

London Gold Shortage

On Wednesday 29 January, the London Financial Times (FT) broke the news that there is a shortage of gold in the London market. In an article titled “Gold stockpiling in New York leads to London shortage” , the FT revealed that the threat of US tariffs and the arbitrage opportunity on COMEX has created an extreme gold shortage where “the wait to withdraw bullion stored in the Bank of England’s vaults has risen from a few days to between four and eight weeks”. What this really means is that bullion bank members of the London Bullion Market Association (LBMA) are struggling to a) borrow enough gold from central banks, and b) withdraw this gold from the Bank of England so as to fly it across the Atlantic ocean to New York.

According to an anonymous gold sector executive quoted by the FT, “people can’t get their hands on gold because so much has been shipped to New York, and the rest is stuck in the queue. Liquidity in the London market has been diminished.”

Liquidity here is a euphemism for availability of gold. Diminished liquidity really means diminished availability, i.e. a shortage of gold in London. But why would there even be a queue if the gold in the London market is allocated and has only 1 owner for each ounce? The answer of course is that it is not 1 owner per ounce. The entire system is a fractional-reserve system of synthetic gold credit.

Even in normal times, what little physical gold that is in the London is ‘spoken for’ in terms of central bank and ETF holdings, and there is a very small ‘float of gold’ available for ‘liquidity’ purposes. And in abnormal times, such as now in an environment of heightened physical demand, that gold float is even smaller.

Not surprisingly, the Bank of England and the LBMA are trying to pretend there is no problem, and are trying to pass off the London gold shortage as logistical bottlenecks. According to a Bank of England spokesperson quoted last week by Marketwatch “there is no shortage of gold”. There are just “longer than usual wait times to get gold transferred out of the Bank of England vaults” due to higher demand. Do the Bank of England clients actually fall for these excuses?

The same article quotes a spokesperson from LBMA member Bullionvault (a frequent LBMA apologist), who tries to convince anyone who will buy it that “digging out physical bullion bars from large vaulted stockpiles takes time, manpower, trucks and transport”. How come this wasn’t a problem when countries such as Venezuela, Poland, Hungary, Serbia, India and Turkey withdrew 100s of tonnes of gold from the Bank of England in recent years and repatriated it to their home countries?

The Bank of England governor Andew Bailey also got in on the denial act, and shockingly, this was in front of the UK Treasury Select Committee on Wednesday 29 January (Full hearing). When asked about US $ 82 billion of gold flowing from London to New York in recent months, Bailey disingenuously avoided the question and responded that “It’s not a big thing really … gold doesn’t play the role it used to play”, before saying “I don’t want to dramatize this story”. However, Bailey’s attempt at downplaying the situation fell flat – his unconvincing performance in his testimony on the gold crisis was a case of amateur dramatics, and he really needs to go to a better acting school. See clip here.

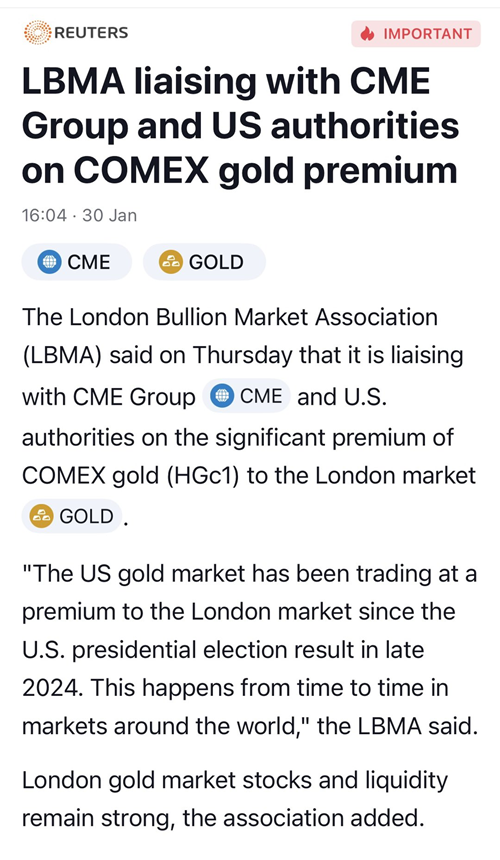

The LBMA also told MarketWatch with a straight face that “London gold market stocks and liquidity remain strong”, but at the same time it said that it was “monitoring and liaising closely with the CME Group and with U.S. authorities”. Reuters also corroborated that the LBMA is discussing the COMEX-London gold premium with the CME and US Authorities.

But why is the LBMA liaising with the CME and US Authorities at all, and intervening in a supposedly free market price setting process? Is it because:

- The LBMA and COMEX are the two leading venues for ‘paper gold price discovery’ and they don’t want the gold price to breakout to real price discovery?

- And that physical gold is a strategic monetary metal which the non-Western countries are now preparing to bring back to the centre of a new future monetary system?

Discussions with the US authorities beg the question, which authorities are the LBMA and CME Group talking to? The CFTC, the US Treasury, the New York Fed, the President’s Working Group on Financial Markets?

All of this sounds similar to 2020, when, during Covid economic lockdowns, the COMEX-London spread blew out, hundreds of tonnes of gold moved from Europe to New York, and the LBMA and the CME Group colluded closely in an attempt to control the gold price. For background see “Bullion Bank Nightmare as LBMA-COMEX Spread Blows Up Again” (9 April 2020), “COMEX Adds 730 Tonnes of Gold Since Late-March” (6 July 2020) and “LBMA-COMEX Collusion Intensifies" (24 August 2020)

On a bigger picture basis, the question has to be asked, why is the LBMA even in charge of the global gold market? In the midst of a gold crisis – which it denies is occurring – the LBMA is a) focusing on a pet hobby gold bar integrity project, b) organising conferences but recovering from getting ripped off by fraudsters, and c) getting sued in London’s High Court in a trial which will take place in June 2026 – See “Trial of the London Bullion Market Association to go ahead at the High Court next year following alleged human rights abuses at African gold mine”.

Is the LBMA even the correct entity to be the world gold market’s self-proclaimed “global authority”?

Mexico and Canada are two of the largest suppliers of gold imported by the United States, both in the form of doré and precipitates, and refined bullion. For example, according to the U.S. Geological Survey monthly gold survey for October 2024, of the 12.1 tonnes of gold imported into the US that month, the top 3 suppliers were Columbia (25% of the total), Mexico (24% of the total) and Canada (13% of the total). The 25% import tariffs imposed by the US on Canada and Mexico will now seriously impact these gold import flows.

US imports of gold and silver from Mexico and Canada

Since the US can no longer import tariff free gold from Canada and Mexico, the US therefore cannot export gold to the UK and Switzerland. This will result in less gold making its way to London, thereby further tightening liquidity in the LBMA market. The only workaround would be for Mexico and Canada to reroute their gold directly to refineries in Switzerland or other locations, bypassing the US entirely. However, this would still create logistical delays and potential dislocations in the global gold supply chain, further pressuring London’s available gold inventory.

Looking at silver, Mexico is the world’s largest silver producer, and according to USGS, Mexico produced 6300 tonnes of silver in 2024 which was 25% of 2024’s total global silver production. China is the world’s second largest silver producer, with 3300 tonnes production in 2024.

Furthermore, Mexico and Canada are the two largest suppliers of silver to the US. For example, in October 2024, which is the latest USGS data available, the US imported 163,000 kgs of silver from Mexico and 92,500 kgs of silver from Canada. With total US silver imports that month of 318,000 kgs, Mexico represented 51% of all silver imports and Canada represented another 29%. So together Mexico and Canada accounted for 80% of all US silver imports. This is a staggering figure and shows how dependent the US is on silver from Mexico and Canada. Imposing a 25% import tariff on Mexican and Canadian silver imports is going to affect the US silver sector in a massive adverse way.

US Strategic Gold Stockpiling

With import tariffs now confirmed and about to be implemented, it will be interesting to see how the COMEX – London spread reacts. If the spread remains elevated for an extended period, it raises the question of how much gold the London market can continue to supply to New York before inventories can’t take it.

A persistent premium would also suggest that this isn’t just short-term arbitrage but the beginnings of a systemic crisis within which there is a larger strategic accumulation effort by the US government under the smokescreen of tariffs, possibly aimed at draining gold liquidity from London and consolidating gold reserves within US vaults, so as to back a US Treasury gold bond, given that there is no evidence that the US Treasury has all the gold it claims to have (as it has never been fully physically and independently audited).

If London’s gold stocks deplete faster than they can be replenished, it could also trigger a supply squeeze, expose weaknesses in the global bullion market, and force a dramatic repricing of physical gold – especially if other central banks or sovereign entities react by accelerating their own gold accumulation out of London.

Recall that central bank gold buying continues to be very strong, both from identified central bank buyers, and unidentified central bank and sovereign wealth fund buyers. The physical gold which the US markets are attempting to hoover up in London and Switzerland also has to compete at the margin, with all of these sovereign buyers, including the Chinese central bank.

BullionStar Inventories

Despite apparent shortages of gold in the London wholesale market, BullionStar maintains adequate bullion inventories of gold and silver coins and gold and silver bars, and offers an uninterrupted supply of bullion for our customers from the world’s leading mints and refineries. We have not seen shortages at the retail level, and customers can purchase physical gold and silver with confidence, knowing that availability remains stable even as global supply constraints arise.

Conclusion

Bizarrely, none of the industry associations in the global precious metals markets, including the the LBMA, World Gold Council, Silver Institute and International Precious Metals Institute, have issued any press releases or pubic statements regarding the 25% import tariffs on gold and silver coming into effect from Mexico and Canada. Nor have the CME Group or the CFTC made any public pronouncements. This silence is surprising, and suggests that these institutions are deliberately avoiding the issue, and leaving market participants and investors in the dark about the implications.

The tariffs on gold and silver imports from Mexico and Canada will have far-reaching consequences:

– Higher domestic gold and silver prices in the US for bullion bars and coins from tariffed countries – due to the 25% tariff.

– Depletion of London’s gold stocks, tightening liquidity in the LBMA market.

– Potential dislocations in the global gold supply chain, especially if Mexico and Canada reroute their gold exports.

– Potentially higher costs for any precious metals miners – since tariffs and retaliatory tariffs by the US, Canada and Mexico could create extra costs and frictions for miners are located in these jurisdictions.

– Strategic US gold accumulation, possibly as a precursor to a future gold-backed financial system.

These developments mirror the 2020 COVID-era gold crisis, where gold flowing rapidly from London to New York and LBMA-COMEX collusion was evident. But the crucial question now is whether the current crisis is just a temporary dislocation, or the start of a larger shift in the global gold market away from paper and towards physical.

This current shortage of gold in London is also further proof that the London ‘gold’ market is primarily a paper market with very fragile underpinnings. It is literally an inverted pyramid where the physical holdings at the bottom underpin the entire gigantic paper edifice. With those physical underpinnings now being taken away, expect subsidence, and expect the LBMA to be frantically searching for a compliant quantity surveyor to sign off that all is ok under the foundations of the LBMA house – when in reality it’s not.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets