SPDR Gold Trust Gold Bars Being Held at the Bank of England

Ronan Manly

Ronan Manly 12 Comments

12 CommentsOne of the most notable developments accompanying the gold price rally of 2016 has been the very large additions to the gold bar holdings of the major physically backed gold Exchange Traded Funds (ETFs). This is especially true of the SPDR Gold Trust (ticker GLD).

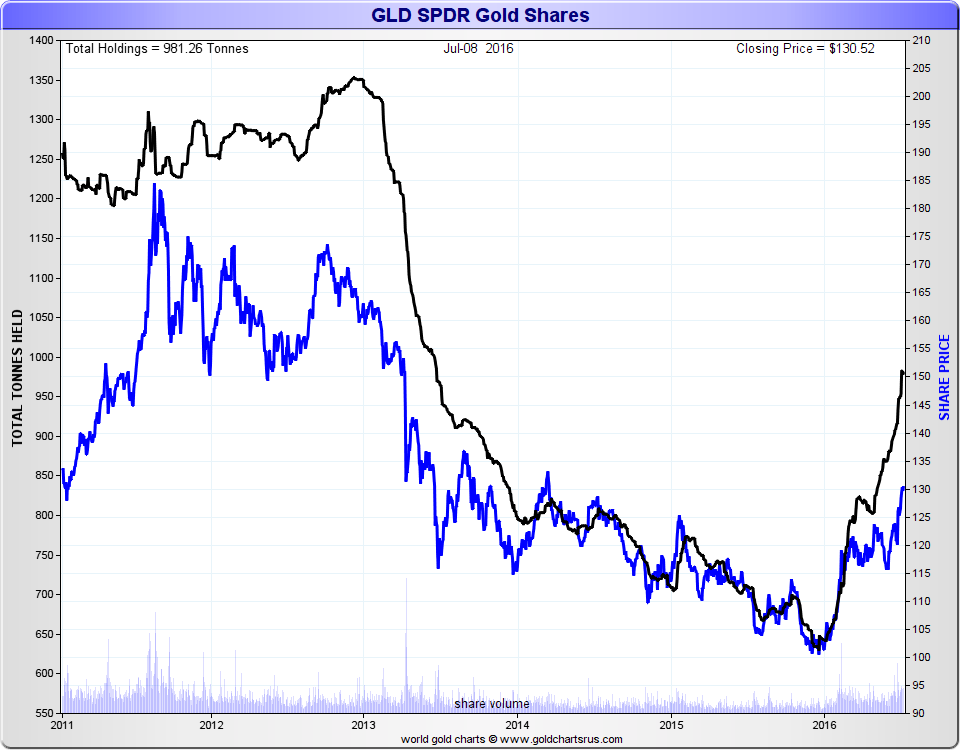

The gold bar holdings of the SPDR Gold Trust peaked at 1353 tonnes on 7 December 2012 before experiencing a precipitous fall in 2013, and additional and continued shrinkage throughout 2014 and 2015. On 17 December 2015, the gold holdings of the SPDR Gold Trust hit a multi-year low of 630 tonnes, a holdings level that had not been seen since September 2008.

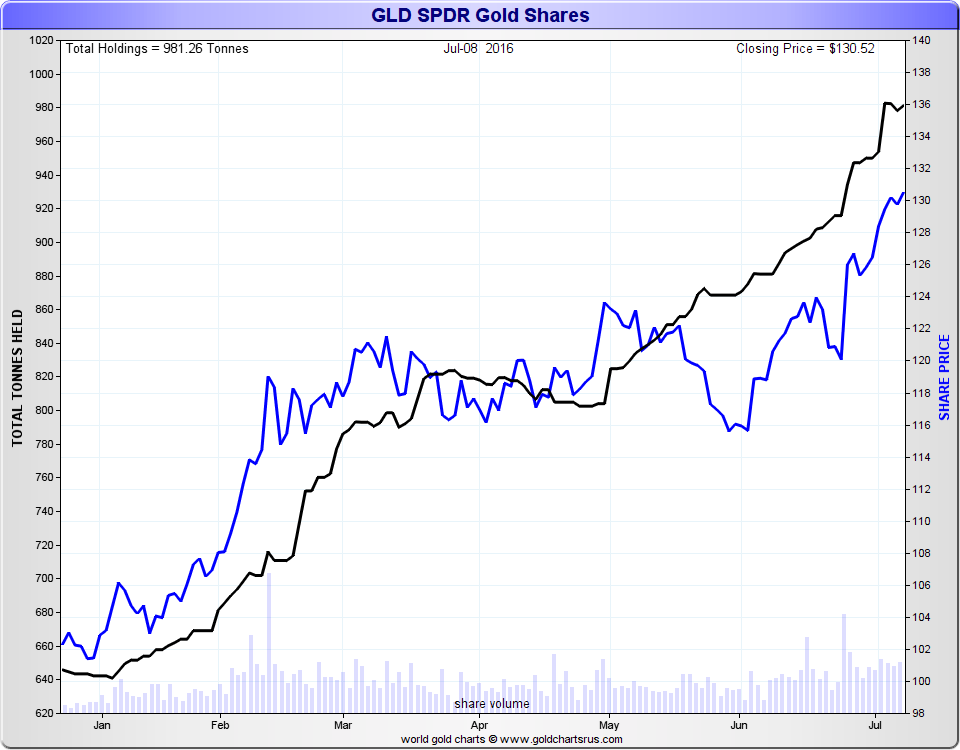

By 31 December 2015, GLD ‘only’ held 642 tonnes of gold bars. See above chart. Then as the New Year kicked off in January 2016, something dramatic happened. The SPDR Gold Trust began expanding its gold holdings again, and noticeably so. By 31 March 2016, the Trust held 819 tonnes of gold bars, and by 30 June 2016, it held 950 tonnes of gold bars. The latest figure at time of writing is 981 tonnes of gold bars as of 8 July 2016. (Source: GLD Gold holdings spreadsheet).

This is a year-to-date net change of 338.89 extra tonnes of gold bars being held within the SPDR Gold Trust. See chart below. That’s a 52.8% increase compared to the quantity of gold bars the Trust held at the end of 2015, and a phenomenal amount of gold by any means, since it’s over 10% of annual new mine supply, and also a larger quantity of gold than all but the world’s largest central banks hold in their official gold reserves. Where is all of this gold being sourced from? That is the billion dollar question. Some is obviously being imported from Swiss refineries, but perhaps not all of it.

In January 2016, 26.8 tonnes of gold bars were added to the SPDR Gold Trust, while a massive 108 tonnes of gold bars were added in February 2016. The first quarter was rounded off with an additional 42 tonnes of gold bars added in March, bringing the Q1 additions held by GLD’s gold custodian HSBC London to 176.91 tonnes of gold bars. Noticeably, some large 1-day increases in GLD’s gold bar holdings occurred on 1 February (over 12 tonnes), 11 February (over 14 tonnes), 19 and 22 February (over 19 tonnes each day), and 29th February (nearly 15 tonnes), and also on 17 and 18 March (11.9 tonnes of gold bars added each day).

The second quarter saw a 15 tonne shrinkage of GLD’s gold holdings in April, but a very large 64.5 tonne increase in May, and a 81.4 tonne increase in June, making for a Q2 increase in GLD’s gold bar holdings of 130.77 tonnes. Very large 1-day gold bar additions occurred on 24 and 27 June (18.4 tonnes and 13 tonnes respectively). Overall, that’s 307 tonnes added to GLD in the first half of 2016.

Adding the 31.2 tonne addition for July to date gives the 338.89 tonnes addition figure quoted above. Most of this was due to a large 1-day inflow of 28.81 tonnes of gold bars reported on 5 July.

SEC – Reveal the subcustodians

I have detailed the above GLD gold bar holding changes to provide some background and put more color on the important discussion which follows.

While looking through SEC filings of the SPDR Gold Trust last month, I came across some interesting correspondence between the SEC and the sponsor of the SPDR Gold Trust, World Gold Trust Services. World Gold Trust Services is a fully owned subsidiary of the World Gold Council (WGC).

On 29 March 2016, the US Securities and Exchange Commission (SEC) sent a letter to the SPDR Gold Trust (c/o World Gold Trust Services, LLC) essentially telling the SPDR Gold Trust to in future specify in its SEC filings the identities of the sub-custodians that are storing any of the Trust’s gold bar holdings during each reporting period. The SEC’s letter stated:

“We understand that the Custodian may appoint one or more subcustodians to hold the Trust’s gold and that the Custodian currently uses a number of subcustodians, identified on page 18. You also outline risks that may arise in connection with the use of subcustodians. In future Exchange Act periodic reports, to the extent material, please disclose the amount of the Trust’s assets that are held by subcustodians.”

The page 18 referred to by the SEC is page 18 of the annual 10-K filing of the SPDR Gold Trust for the year ended 30 September 2015, which includes the following paragraph:

“The Custodian is authorized to appoint from time to time one or more subcustodians to hold the Trust’s gold until it can be transported to the Custodian’s vault. The subcustodians that the Custodian currently uses are the Bank of England, The Bank of Nova Scotia-ScotiaMocatta, Barclays Bank PLC, JPMorgan Chase Bank and UBS AG.

In accordance with LBMA practices and customs, the Custodian does not have written custody agreements with the subcustodians it selects. The Custodian’s selected subcustodians may appoint further subcustodians. These further subcustodians are not expected to have written custody agreements with the Custodian’s subcustodians that selected them. The lack of such written contracts could affect the recourse of the Trust and the Custodian against any subcustodian in the event a subcustodian does not use due care in the safekeeping of the Trust’s gold. See “Risk Factors—The ability of the Trustee and the Custodian to take legal action against subcustodians may be limited.”

LBMA above refers to London Bullion Market Association. Note that the SPDR Gold Trust prospectus defines subcustodian as:

“SUB-CUSTODIAN means a sub-custodian, agent or depository (including an entity within our corporate group) selected by us to perform any of our duties under this agreement including the custody and safekeeping of Bullion.”

The SEC letter was addressed to William Rhind who was CEO of World Gold Trust Services, but who actually had resigned as CEO on 9 February 2016, something the SEC should have known since the resignation statement was also filed with the SEC. After receiving the SEC’s correspondence, Samantha McDonald, CFO of World Gold Trust Services, responded by letter to the SEC the next day, 30 March 2016, confirming that:

“We will, to the extent material, disclose in future periodic reports the amount of the Trust’s assets that are held by subcustodians. Please be advised that during fiscal 2015, no gold was held by subcustodians on behalf of Trust.

Note that filings with the US SEC use the naming convention 10-K for an annual filing, and 10-Q for a quarterly filing.

Following the stipulation from the SEC to World Gold Trust Services telling it to reveal its subcustodian holdings, its intriguing to note that when SPDR Gold Trust filed its next 10-Q on 29 April 2016 for the quarter ended 31 March 2016, page 15 of this filing revealed that the Bank of England, as subcustodian, had, during Q1 2016, held up to 29 tonnes of gold on behalf of the SPDR Gold Trust. The relevant section of page 15 stated the following:

“As at March 31, 2016, the Custodian held 26,484,117 ounces of gold on behalf of the Trust in its vault, 100% of which is allocated gold in the form of London Good Delivery gold bars including gold payable, with a market value of $32,760,852,177 (cost — $32,291,685,964) based on the LBMA Gold Price PM on March 31, 2016. Subcustodians held no gold on behalf of the Trust as of March 31, 2016.

During the quarter ended March 31, 2016, the greatest amount of gold held by subcustodians was approximately 29 tonnes or approximately 3.8% of the Trust’s gold at such date. The Bank of England held that gold as subcustodian.

As at September 30, 2015, the Custodian held 21,995,797 ounces of gold in its vault 100% of which is allocated gold in the form of London Good Delivery gold bars including gold payable, with a market value of $24,503,317,923 (cost — $27,103,546,125). Subcustodians held nil ounces of gold in their vaults on behalf of the Trust.”

Some Facts

From the above revelations, some facts can be stated:

- The Bank of England held a maximum of 29 tonnes of gold on behalf of the SPDR Gold Trust on some date during Q1 2016.

Note that the wording of the 10-Q is such that it does not preclude the possibility that the Bank of England also held GLD gold at other times during Q1 2016, since it states “the greatest amount of gold” that the Bank of England held for the Trust was 29 tonnes. This implies that the Bank of England vaults could, at other times during Q1, have held less than 29 tonnes of gold on behalf of GLD.

- As per the initial WGTS response to the SEC dated 30 March 2016, no gold was held by HSBC’s subcustodians on behalf of GLD throughout fiscal 2015 (1st October 2014 – 30 September 2015). Furthermore, GLD’s 10-Q to 31 December 2015 states that

To this can be added that according to the SPDR Gold Trust’s 10-Q for Q4 2015, “as at December 31, 2015…Subcustodians held nil ounces of gold in their vaults on behalf of the Trust”

The GLD 10K (annual) for the year to 30 September 2015, filed on 24 November 2015, also contains a few statements addressing whether gold was held by subcustodians on year-end dates in 2014 and 2013. However, it states that subcustodians did not hold gold on behalf of the SPDR Gold Trust on these two dates. Page 44 states:

“As at September 30, 2014, the Custodian held 24,867,158 ounces of gold in its vault 100% of which is allocated gold in the form of London Good Delivery gold bars including gold payable, with a market value of $30,250,898,159 (cost — $30,728,152,437). Subcustodians did not hold any gold in their vaults on behalf of the Trust.”

As at September 30, 2013, the Custodian held 29,244,351 ounces in its vault 100% of which is allocated gold in the form of London Good Delivery gold bars including gold payable, with a market value of $38,792,631,793 (cost — $35,812,777,235). Subcustodians did not hold any gold in their vaults on behalf of the Trust."

How did Bank of England suddenly become a GLD subcustodian in Q1 2016?

As a member of London Precious Metals Clearing Limited (LPMCL), HSBC maintains gold bullion account facilities at the Bank of England which can be used within its LPMCL gold clearing role. All 6 LPMCL bullion bank members hold gold accounts at the Bank of England. The 6 LPMCL members can also all call on each other for physical delivery of gold and allocation of gold. All of these bullion banks except ICBC Standard are also Authorized Participants (APs) of GLD, i.e. Barclays, HSBC, JP Morgan, Scotia, and UBS. Other AP’s of GLD include entities of Credit Suisse, Goldman Sachs, Merrill Lynch and Morgan Stanley. Many of these bullion banks are also LBMA market makers in gold.

My view is that quite a number of other bullion banks that are members of the LBMA also hold gold accounts at the Bank of England, such as BNP Paribas, Natixis, SocGen and Standard Chartered, otherwise they would not be able to engage in the gold borrowing activities that they are on record of engaging in. If this is the case, then gold bars can easily be moved from central bank accounts at the Bank of England to bullion bank gold accounts at the Bank of England and vice-versa. Only APs of GLD are allowed to create baskets of GLD securities. This creation process requires that when GLD baskets created, APs have to deliver physical gold bars to HSBC.

There are therefore a number of possibilities to explain how the Bank of England ended up being a sub-custodian for GLD in Q1 2016.

- An AP(s) had gold bars stored at the Bank of England, and delivered these gold bars to HSBC at the Bank of England in fulfillment of the GLD share creation process

- An AP(s) had an unallocated credit balance of gold with a LPMCL clearer or other entity which had gold stored at Bank of England or access to gold at the Bank of England, and as part of the clearing process the AP converted unallocated credit balances into allocated gold bars held at the Bank of England and delivered these gold bars to HSBC.

- An AP(s) borrowed gold from a central bank which had gold bars stored at the Bank of England and delivered these gold bars to HSBC as part of the GLD basket creation process.

The quantity of 29 tonnes is a lot of gold for an Authorized Participant or group of APs to have un-utilised in a vault at the Bank of England. It’s about 2320 large Good Delivery gold bars. Likewise, 29 tonnes is a lot of gold bars for LPMCL members to have as a clearing float at the Bank of England.

Furthermore, if an AP had acquired newly refined gold from a refinery with the intention of delivering it to HSBC as part of the GLD security creation process, why would this gold be delivered to the Bank of England vaults, and not directly to the HSBC vault? It would be more practical to have delivered that gold straight to the HSBC vault.

Therefore, its plausible that at least some of the gold being held by the Bank of England as sub-custodian on behalf of the SPDR Gold Trust was sourced from gold borrowed from central bank gold holdings at the Bank of England.

Bullion Bars Database

There is further support for borrowed gold bars being held by the SPDR Gold Trust during Q1 2016.

Warren James maintains a database of the identities of the gold bars held in the GLD over time which allows comparisons between the gold bullion coming in and out of the GLD. Each bar has a unique signature based on its brand, serial number, and weight. Gold bars coming into the SPDR Gold Trust can be tracked based on whether these bars were previously held in the Trust or whether they are bars coming in that have never been held by the Trust before. When a bar returns to the list after it was previously held but disappeared from the holdings, it’s called dark bullion since its identity is familiar but it’s not known where the bar has been since it left the GLD and re-entered.

Up until 10 February 2016, the percentage of dark bullion bars re-entering GLD that had previously been held by the Trust was about 30% of the inflows. As the inflows into GLD rose sharply from the second half of February, dark bullion entering GLD essentially stopped and nearly all of the bars being added to GLD were bars that had never been held by GLD before. These inflows were a combination of newly refined gold and older bars which are no longer produced. For example, gold bars coming into GLD in February 2016 have included hundreds of bars from the US Assay Offices and Mints, AGR Matthey, Johnson Matthey Plc (Royston), the Australian Branch Royal Mint – Perth, Engelhard, Kazzinc etc, all of which are no longer produced.

The fact that a large amount of older gold bars arrived into GLD from the second half of February onwards would suggest that these bars came long-held holdings in the vaults of the Bank of England, and consisted of borrowed central bank gold.

Some Questions

All of the above poses a number of questions:

If this known 29 tonnes of gold was held by the Bank of England as subcustodian for GLD during Q1 2016 but not held by the Bank of England as subcustodian at the end of March 2016, did it physically leave the Bank of England vaults, or was it just transferred to HSBC’s account at the Bank of England?

Note that nothing in the SEC filing rules or directives compels WGTS to specify if the GLD custodian HSBC is holding gold outside its own vaults, so in my view its possible that gold is held by HSBC on behalf of the SPDR Gold Trust at the Bank of England. Indeed, its possible that HSBC even leases vault space in the Bank of England vaults, a sub-leased vault facility. If the HSBC London gold vault is indeed in the location that’s documented here (HSBC’s London Gold Vault: Is this Gold’s Secret Hiding Place?), then it would appear that it’s not big enough to accommodate the entire gold bar holdings of GLD and all other HSBC customers’ gold, especially when GLD holding are and were over 900 tonnes.

Since the Bank of England didn’t hold any gold as subcustodian for GLD in fiscal 2015, but did in Q1 2016, how much of these large inflows of gold into GLD in Q1 and Q2 and July this year (documented above) involved metal stored in vaults at the Bank of England? And what changed in the London Gold Market to require gold held at the Bank of England to suddenly be needed to fulfill GLD gold delivery obligations?

Why are LBMA practices and customs so lax that it allows HSBC the custodian, not to have written custody agreements with the subcustodians. Surely the US SEC should have picked up on this?

Why did the SEC not ask iShares (IAU (which has 3 custodians) and ETF Securities to also alter their SEC filings to reveal subcustodians’ holdings. And for that matter why did the SEC not ask iShares to amend its disclosures to specify subcustodians in the Silver ETF – SLV.

Why do central banks never publish gold bar lists detailing the serial numbers of their bars, and why is the Bank of England so against allowing central banks to do so. There are a number of FOIA requests (including one I made) providing evidence of the Bank of England’s refusal to allow central banks to publish weight lists / bar lists. Could it be that they do not want data on gold bar serial numbers entering the public domain as it would then show that leased and swapped gold is being held by commercial gold ETFs?

Audits of the SPDR Gold Trust’s gold bars

The SPDR Gold Trust ‘s gold bar holdings are physically audited twice per year. A partial physical audit is conducted in February/March of each year, and a full physical audit of the bars is done in September of each year. The current auditor is Inspectorate International Limited. In September 2015, Inspectorate conducted the 2015 full count of the Trust’s gold bullion held by the custodian HSBC London. That audit counted 54,807 London Good Delivery gold bars at the “London Vaults of HSBC Bank USA National Association". Note that the official custodian of the SPDR Gold Trust changed from HSBC Bank USA to HSBC Bank Plc in late 2014, so this audit should really state HSBC Bank Plc.

Inspectorate then conducted a random sample count audit in early Mach 2016 at the “London Vaults of HSBC Bank Plc" based on a date of 19 February 2016. As of that date, the “account (GLD) held title to 56,913 London Good Delivery, large Gold Bars“. However, this audit was “a statistically random count of 16,493 bars of gold", based upon the gold inventory as at 19 February 2016, and it was carried out between 29 February and 11 March “at the Custodian’s premises“.

Given that the Bank of England acted as a subcustodian to the SPDR Gold Trust during Q1 2016, the question arises as to whether all of the other 40,420 (56,913 – 16,493) bars were at the “Custodian’s premises” during the audit, or were some of these other bars being held in the Bank of England vaults. It’s not clear why a random sample of 16,493 bars (about 206 tonnes, and 29% of the total holding) was chosen, but it’s about 2/7ths of the gold bars held by GLD.

There is no mention of the Bank of England in Inspectorate’s latest audit report. However, there is nothing to say that some of GLD’s bars were not in the Bank of England at the time of the audit. The audit doesn’t say so one way or the other, and the way its worded means that it doesn’t say all of the inventory is at HSBC’s vault, just that the audit was conducted at HSBC’s vault.

Conclusion

Central banks continue to report leased and swapped gold (gold receivables) as an asset on their balance sheets. This accounting fiction, which doesn’t follow any international accounting standards is a sleight of hand that allows the same gold to appear to be in two places at once. If gold bars that have been leased from central banks are being held in the SPDR Gold Trust, then these gold bars are being double-counted, and GLD shareholders should be made aware that the Trust is holding gold that has been ultimately borrowed from central banks. Using borrowed central bank in an ETF doesn’t put the ETF on the hook, since the ETF owns this gold. But it does mean that the bullion banks will need to return the equivalent amount of borrowed gold to the lending central bank from other sources. Importantly though, this type of activity will overstate the amount of gold held by the combined official sector and ETF sector.

The SPDR Gold Trust 10-Q for the 2nd quarter of 2016 will be filed with the SEC in about 3 weeks time, at the end of July. With the continuing large inflows into GLD in Q2 2016 it will be interesting to see whether the name of Bank of England as subcustodian of GLD reappears in the Q2 filing?

And if gold bars held by GLD are actually stored at the Bank of England vaults when the full physical gold bar audit is conducted next September, surely the full audit report should require a passage stating that some of the gold bars audited were held at the Bank of England, and not just at the ‘London Vaults of HSBC Bank’? Since the SEC have opened this ‘can of worms’ issue, and created more questions than answers, perhaps it is now in the SEC’s interests to go even further and ask World Gold Trust Services to fully clarify the matters raised above. Otherwise, the GLD gold bar holdings will continue to be a source of intrigue and debate in the gold world.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

Gold at All Time Highs amid Physical Gold Shortages

Gold at All Time Highs amid Physical Gold Shortages